.png)

Canada’s Surprising GDP Rebound—and What It Signals for the Aluminum Market

- Harrison Shrair

- Dec 1, 2025

- 3 min read

Canada’s economy snapped back faster than expected in the third quarter, showing a sharp pivot in growth drivers that carries important implications for global metals markets—especially aluminum.

Statistics Canada reported that GDP rose at a 2.6% annualized rate, the strongest pace since late last year and a full reversal of the 1.8% contraction in Q2, when a collapse in goods exports—triggered by U.S. trade actions—pulled the economy downward.

Economists projected only a 0.5% increase. Canada instead delivered a housing- and government-driven rebound that masks underlying weakness in exports, business investment, and industrial output.

Housing & Government Spending Fuel the Rebound

Residential investment jumped 6.7% annualized, powered by a resurgence in housing resales. At the same time, federal spending—particularly on defense systems and military assets—added significant lift. With Prime Minister Mark Carney committing billions in new military investment to meet NATO benchmarks, defense will likely remain a key GDP booster into 2025.

Monetary policy is supportive, too. With the Bank of Canada’s policy rate at 2.25%—slightly stimulative—housing activity continues to enjoy tailwinds despite economic uncertainty.

Exports Still Struggling Post-Tariffs

Exports grew only 0.7% in Q3, hardly recovering from the 25% plunge in Q2 when the U.S. levied tariffs on Canadian imports. Crude oil and bitumen provided some relief, but manufacturing exports remain weak.

Imports dropped a dramatic 8.6%, the largest decline since 2022, reflecting falling domestic demand and lower shipments of high-value unwrought metals (gold, silver, platinum).

Rising Pessimism Among Consumers & Businesses

Household consumption declined 0.4%, the first drop since 2021. Final domestic demand fell 0.1%. Canadians are spending less and saving more as uncertainty grows.

Business sentiment is similarly subdued:

Non-residential investment fell 4.5%

Machinery and equipment orders declined

Companies liquidated nearly C$4 billion in inventories

Industrial GDP is estimated to have dropped 0.3% in October

These indicators suggest the Q3 rebound may be short-lived.

What This Means for the Metals Market—Especially Aluminum

Even though metals weren’t the primary catalyst for the Q3 rebound, the underlying economic shifts are reshaping the aluminum market in real time.

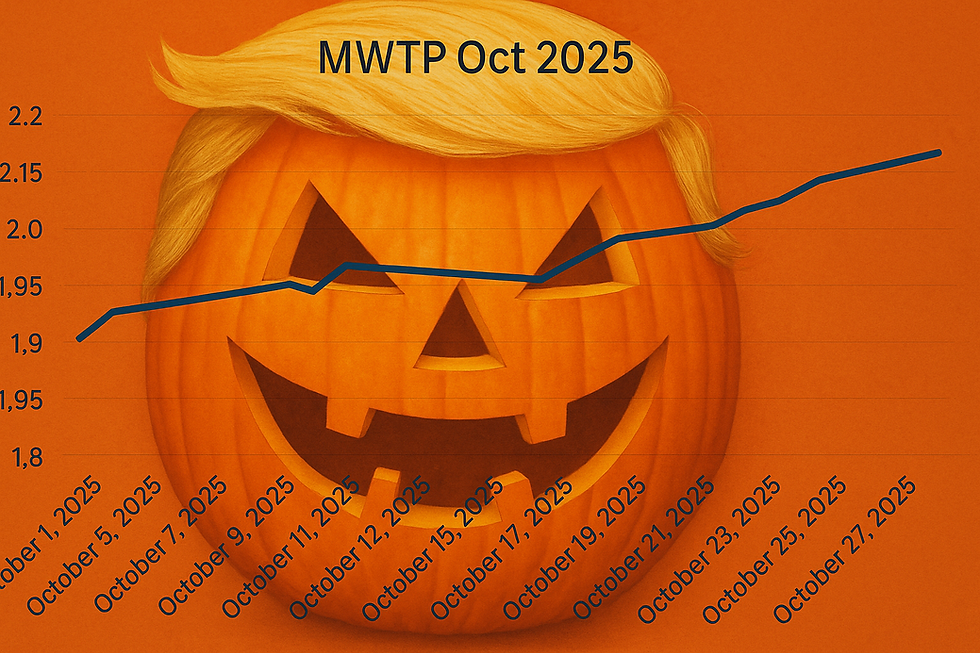

1. Aluminum Market Surges Nearly 4 Cents Since the Day Before U.S. Thanksgiving

Despite broader economic softness, aluminum pricing has strengthened noticeably:

LME Aluminum increased from $1.265 to $1.2968, a jump of 3.68¢

Midwest Premium rose from $0.8725 to $0.8805, up 0.80¢

Combined, the move represents nearly a 4-cent surge in the aluminum market in just a matter of days. This upward pressure signals tightening supply conditions—likely driven by reduced imports, cautious mill buying strategies, and uncertainty stemming from ongoing U.S.-Canada trade dynamics.

This price action is particularly impactful for scrap processors and traders, as spreads on UBCs, RSI, cast, and extrusion grades react quickly to LME + MWP movements.

This rise should be taken with a grain of salt, as US domestic buying prices have either remained the same from last week or have even dropped. As we've seen in the past, when the aluminum market rises, the mills widen their spreads.

2. Industrial Weakness Softens Demand for Certain Grades

Canada’s failing industrial output means lower demand for:

6063 & 6061 extrusions

EC wire

RSI-dependent alloys

MLC and industrial sheet

A 0.3% drop in industrial GDP for October reinforces expectations of softer mill demand through early 2025.

3. Housing Strength Supports Construction-Grade Scrap

The 6.7% surge in residential investment boosts:

Siding

Old Sheet & MLC

Renovation-driven UBC flows

Residential wiring and mixed low-copper aluminum

While not enough to offset industrial weakness, it provides needed stabilization to scrap markets and helps keep certain grades afloat.

4. Defense Spending Drives Primary Demand, Indirectly Tightening Scrap Supply

Military procurement—vehicles, components, aerospace materials—can tighten the availability of:

Primary billet

RSI

Certain wrought alloys used in defense manufacturing

This indirect supply pressure helps support pricing for higher-grade scrap, especially clean extrusions and segregated alloys.

5. Falling Imports Could Tighten Domestic Aluminum Supply Further

With imports dropping 8.6%, if even a portion of that decline extends into aluminum, mills may rely more heavily on domestic scrap streams.

This dynamic can:

Increase competition for clean grades

Strengthen the floor on UBC pricing

Reduce the availability of cast-grade feedstock

Combined with the LME/MWP rally, these supply pressures may keep aluminum values elevated into early 2025—even if industrial demand remains soft.

Bottom Line

Canada’s Q3 rebound paints a picture of an economy supported by policy choices—not organic growth. For the aluminum market, the implications are even more nuanced:

Prices are rising sharply (nearly 4 cents since pre-Thanksgiving)

Industrial demand is weakening

Housing and defense are providing selective strength

Supply-side tightening may continue

Trade uncertainty is amplifying volatility

As 2025 approaches, aluminum traders, processors, and mills must navigate a market defined by conflicting forces: soft demand, firm pricing, and unstable policy dynamics.

For more insights into the Aluminum market, and for pricing updates, email WF@labrecy.com

(Resources include Bloomberg, Bank of Canada, Marex, Argus, Reuters)

Comments